{kind=link}

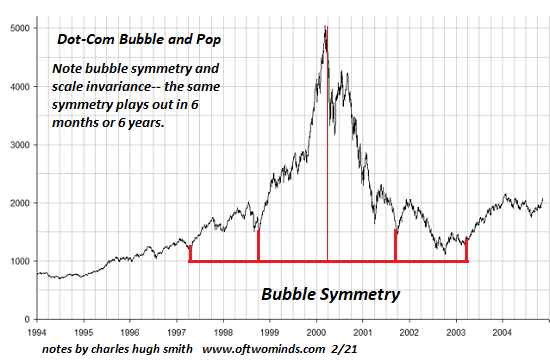

Ultimately policy-makers turn the dials to 11 and nothing takes place.

Lots of others have actually described why inflation is part-and-parcel of the status quo. In the simplest terms, where’s why inflation is important:

1. Our economy and monetary system are absolutely depending on the expansion of credit/debt. Banks make money by issuing brand-new loans, and investors earn money by purchasing and offering financial obligation and instruments that leverage financial obligation. Consumers can just buy big-ticket items with credit.

As a thought experiment, let’s consider what would occur to the United States economy and monetary system if credit was banned and the economy was a cash-only marketplace. The federal government could not run deficits by obtaining money, no one could purchase a vehicle except with money, banks might no longer provide $19 of brand-new loans for every $1 of cash they held.

We all know what would happen: the economy and monetary system would both crash. Envision the scaries of living solely on revenues and having to laboriously conserve up cash to purchase a cars and truck or house.

2. the problem with credit/debt is it accumulates interest. The more we obtain, the more interest we owe. If our earnings doesn’t increase, at some time all our discretionary earnings– what’s left over after paying taxes and fundamentals– is dedicated to debt service, and we can’t borrow more. At that point, the economy slides into recession.

3. There are a few policy escapes of this built-in limitation on the expansion of credit/debt:

A. The government can obtain trillions of dollars and provide every bottom-80% home money to invest. The problem here is the federal government financial obligation likewise accumulates interest, and eventually this crimps federal government loaning and spending.

B. The reserve bank can reduce rates of interest to near-zero so consumers can maximize income by re-financing old financial obligation at substantially lower interest rates.

C. The reserve bank can greatly increase the issuance of currency and credit (a.k.a. “liquidity”) to produce inflation by broadening the quantity of currency and credit chasing goods and services.

Inflation slowly minimizes the burden of debt by raising earnings while keeping the financial obligation the same. For example, back when $2,000 a month was a good salary, a $600/month house mortgage positioned a rigorous limit on the family’s spending.

Fast-forward two decades of “modest” inflation and the typical full-time wage has actually doubled to over $4,000 a month. Voila, the home loan payment has actually stayed the very same (or maybe been minimized via refinancing) and now the $600 regular monthly nut isn’t much of a burden. In truth, the regular monthly nut for the brand-new pick-up truck is larger than the home mortgage.

In a truly steady-state economy, salaries would only rise with boosts in productivity. With performance boosts dawdling along around 1% per year, that’s a modest and unevenly dispersed increase in incomes. Systemic inflation is a lot more trustworthy and broad-based way of reducing the problems of existing debt.

A back-of-the-envelope calculation based upon main inflation is that 2/3 of the wage increases are inflation-driven and maybe 1/3 or less is the result of increasing efficiency.

We now see why inflation is absolutely essential to a credit-dependent economy and financial system. Without inflation, customers and the state quickly max out their income and are unable to obtain and invest more.

What about savers, you ask? They’re sacrificed to support inflation’s disintegration of the currency’s value. As soon as interest rates have actually been suppressed to allow more loaning and costs (referred to as monetary repression), savers are not able to stay even with inflation unless they take on the threats of hypothesizing in stocks, real estate, collectibles, etc.

Financial repression in service of maintaining inflation undoubtedly fuels speculation. The consistent drip of inflation in a low-interest period forces everyone to take on dangers that few are prepared to handle.

Inflation penalizes the citizens in two ways: it deteriorates the worth of their labor, the main source of their income, and it requires them to bet in speculative bubbles where the super-wealthy hold all the high-value cards.

However without inflation, the economy and financial system collapse. So the sluggish erosion of the bottom 80% is a systemic expense of preserving the credit-dependent economy and financial system. The dependence on inflation to keep credit expanding generates winners and losers, but hey, possibly you’ll win huge at the stock exchange live roulette wheel.

This dependence on speculation to keep up with inflation has another pernicious repercussion: it incentivizes the diversion of capital and talent into speculation rather than into financial investments that increase productivity. So while capital chases the stock market chimera of AI, the nation’s creaky, outdated electrical grid that is the structure of whatever fantasy-economy speculators are betting on advances its path to breakdown.

However nothing in the financial world is ever long-term, therefore eventually international threats rise and capital demands a return above absolutely no. This presses bond yields and the expenses of credit greater, crimping borrowing. The profligate growth of currency and credit likewise eventually produce real-world inflation as scarcities fulfill monetary growth: excessive “cash” is going after a constrained amount of items and services.

As soon as inflation heats up, the system starts breaking down as skyrocketing rates of interest suppress borrowing. Central banks and personal banks can issue brand-new credit, but if few can afford to obtain more, the economy spirals into economic crisis.

With rates increasing, the income pump of refinancing is shut down.

The “Goldilocks” economy of the past 30 years was enabled by the deflationary forces of globalization and the huge expansion of credit, a.k.a. financialization. Both of these have topped out and are reversing. Globalization is no longer decreasing costs and everything under the sun has actually already been commoditized and financialized. There disappears swimming pools of “complimentary money” (or totally free anything) waiting to be exploited.

Real-world inflation is crimping discretionary costs, leaving less to service additional loaning. Post-pandemic “vengeance” splurging has diminished savings, and given that all speculative bubbles ultimately pop, the inescapable collapse of the Everything Bubble will kick the reverse wealth impact into high gear.

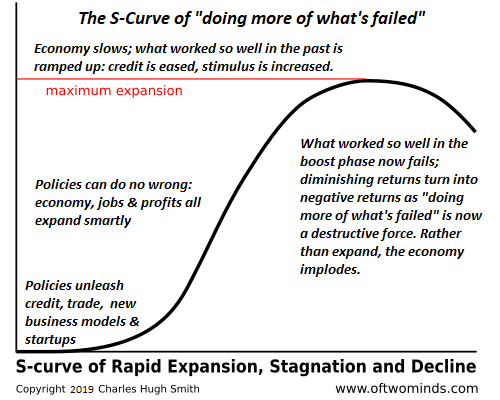

In summary, here’s the issue: the system just functions with Goldilocks moderate inflation however that is no longer possible given the altering tides of globalization, financialization, real-world inflation and rising worldwide threats. This leaves those in charge of the status quo system that benefits the couple of at the expense of the lots of without any sustainable alternative aside from doing more of what’s stopped working until it stops working stunningly.

Put another way, distorting the entire economy and monetary system with monetary repression has actually produced decades of false signals: the system is permanent and sustainable, policies stay effective forever, we can “grow our escape of any issue,” and so on.

Ultimately policy-makers turn the dials to 11 and nothing takes place. Their apparently god-like powers are revealed as mere trickery once the real-world intrudes. What were taken as strong signals turn out to be noise.

My new book is now offered at a 10 % discount rate( $8.95 ebook, $18 print): Self-Reliance in the 21st Century. Read the first chapter totally free(PDF)Check out excerpts of all 3 chapters Podcast with Richard Bonugli: Self Reliance in the

21st Century( 43 min )My recent books

: The Asian Heroine Who Seduced Me( Novel )print$10.95, Kindle$ 6.95 Read an excerpt for

totally free(PDF) When You Can’t Go

On: Burnout, Numeration and Renewal $18 print , $8.95 Kindle ebook; audiobook Read the first section free of charge(PDF)International Crisis , National Renewal: A (Revolutionary

)Grand Technique for the United States(Kindle $9.95, print $24, audiobook)Read Chapter One for free(PDF). A Hacker’s Teleology: Sharing the Wealth of Our Shrinking World(Kindle$8.95, print$20, audiobook$17.46)Check out the first section for free (PDF ). Will You Be Richer or Poorer?: Profit

, Power, and AI in a Traumatized World(Kindle$5, print$10, audiobook)Read the first section for free(PDF). The Experiences of the Consulting Theorist: The Disappearance of Drake(Unique)$4.95 Kindle, $10.95 print); checked out the very first chapters for

complimentary(PDF)Cash and Work Unchained$6.95 Kindle, $15 print)Read the very first area totally free Become a $1/month customer of my work via patreon.com. Sign up for my Substack for free KEEP IN MIND: Contributions/subscriptions are acknowledged in the order got. Your name and email stay private and will not be provided to any other individual, business or firm. Thank you, Pedro M.G.($5/month), for your marvelously generous membership to this site– I am considerably honored by your assistance and readership. Thank you, John K.A. ($ 55.55), for your splendidly generous contribution to this site– I am significantly honored by your steadfast assistance and readership. Thank you, Sebastian S.

($40 ), for yet another superbly generous contribution to this site– I am significantly honored by your steadfast assistance and readership . Thank you, Craig W.($54), for your remarkably

generous contribution to this site– I am greatly honored by your support and readership.