{kind=link}

Although many don’t realize it, interest rates are simply the price of money.

And they are the most important prices in all of capitalism.

They have an enormous impact on banks, the real estate market, and the auto industry. It’s hard to think of a business that interest rates don’t affect in some meaningful way.

Today, we are on the cusp of a rare paradigm shift in interest rates. Such changes take decades—or even generations—to occur. But when they do, the financial implications are profound.

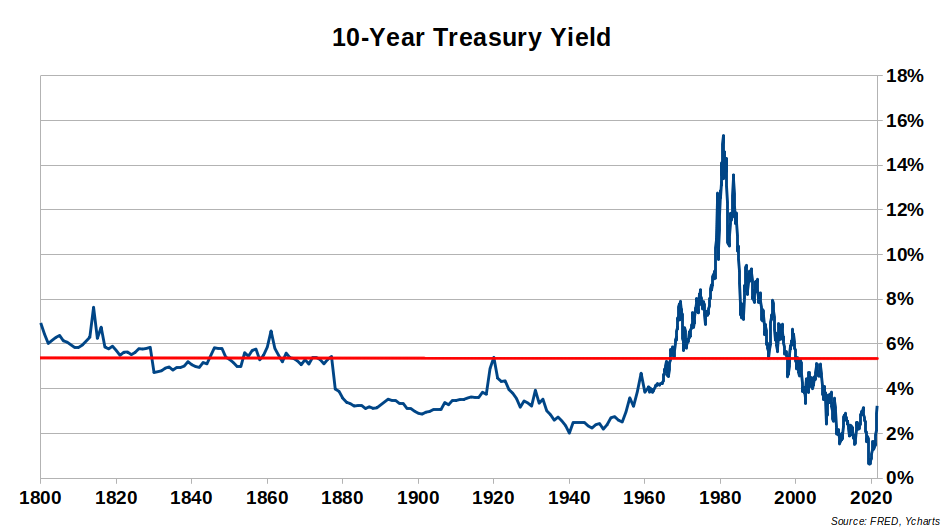

Interest rates rise and fall through decades-long cycles, as seen in the chart below.

That makes sense, as debt is naturally cyclical. It allows people to consume more than they produce now. But it also forces them to produce more than they consume later to pay it off.

Interest rates last peaked in 1981 at over 15%. Then, they fell for 39 years and bottomed in July 2020 at around 0.62%.

The red line marks the long-term average of 5.6%.

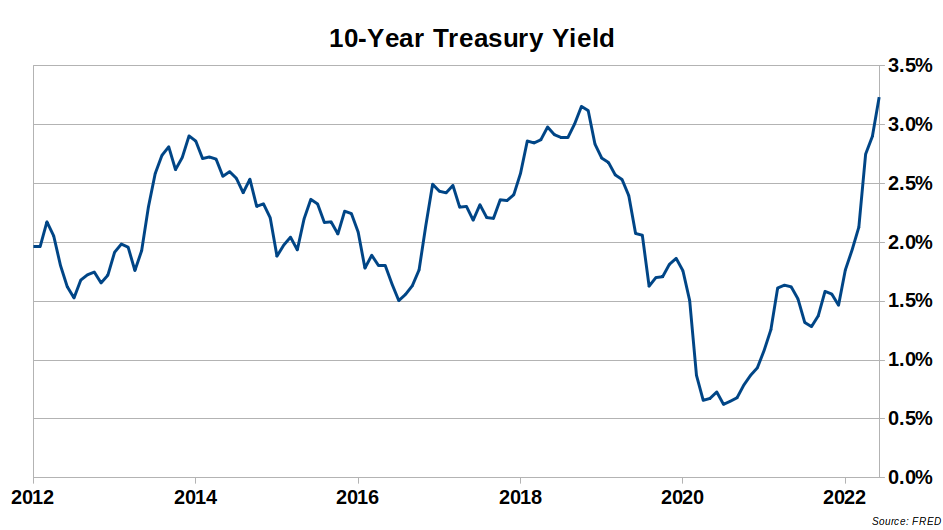

Since the bottom in 2020, yields have gone up more than 5x. This reflects a significant shift. I think we are now at the very beginning of a new, long-term uptrend in interest rates.

As of writing, the 10-year Treasury is yielding around 3.2%. That’s still far below the long-term historical average of approximately 5.6%. It’s also not even in the ballpark of the US government’s dubious official inflation rate of 8.6%, which is undoubtedly understated.

In other words, interest rates have a lot of room to go up.

I expect interest rates to reach new all-time highs in this new, long-term cycle. That would mean we’d see the 10-year Treasury yield north of 15%.

Interest Rates Are Rigged

Remember, interest rates are the price of money. They are the most important prices in all of capitalism. Yet they’re controlled by a politburo of central planners at the Federal Reserve, not set by the market like any other price.

It’s strange that many people thoughtlessly accept this as “normal.” In reality, the Fed is engaged in a massive price-fixing scam… and nobody seems to care.

While the Fed exercises undue influence over interest rates, other significant factors are at play here. And they all point to higher interest rates.

Together, they’re ushering in a once-in-a-generation shift that is both unstoppable and imminent.

Aside from the Federal Reserve, the US government’s federal budget has enormous influence over interest rates. That’s because when the government spends more than it brings in from taxes, it issues debt (i.e., Treasuries) to make up the difference.

And now that Congress has normalized multi-trillion dollar federal spending deficits, that means an avalanche of new Treasuries to finance them.

Who Will Buy All This Paper?

Historically, there has been a vast foreign appetite for Treasuries. But not anymore.

In the wake of Russia’s invasion of Ukraine, the US government has launched its most aggressive sanctions campaign ever.

As part of this, the US government seized the US dollar reserves of the Russian central bank—the accumulated savings of the nation.

It was a stunning illustration of the dollar’s political risk. The US government can seize another sovereign country’s dollar reserves at the flip of a switch.

The Wall Street Journal, in an article titled “If Russian Currency Reserves Aren’t Really Money, the World Is in for a Shock,” noted:

“Sanctions have shown that currency reserves accumulated by central banks can be taken away. With China taking note, this may reshape geopolitics, economic management and even the international role of the U.S. dollar.”

China is one of the largest holders of US Treasuries, and it indeed took note of what happened to Russia. It’s probably a big reason Beijing cut its Treasury holdings to a 12-year low.

Even US allies, like Japan, have also cut their Treasury holdings.

There are numerous other examples. But it’s clear the world isn’t hungry for US debt right now.

The Russia sanctions episode is a reason foreigners—and other Treasury holders—may start to question the US’ willingness to meet its debt obligations. That would drive demand for higher yields to account for the added risk.

What about the Fed?

Usually, the Federal Reserve would help the federal government finance its deficits by creating trillions of new currency units to buy Treasuries. But with inflation spiraling out of control and the Fed desperately tightening, it is not in a position to come to the rescue this time.

To summarize, here are the five reasons to expect higher interest rates:

- Inflation is out of control. Even the government’s official inflation statistics—which understate the situation—are far above current interest rates.

- The federal government must issue a flood of new Treasuries to finance multi-trillion dollar deficits—which are here to stay.

- Sanctions are eroding confidence in the US financial system.

- Foreigners aren’t buying as many Treasuries.

- The Fed is tightening.

When you connect all the dots, I think it’s clear we are starting a new long-term cycle, with rising interest rates and a bear market in bonds. That will have enormous implications for the economy and the stock market.

We will likely see incredible volatility in the financial markets as thousands of businesses that had become accustomed to easy money and artificially low interest rates go bankrupt.

Editor’s Note: The economic trajectory is troubling. Unfortunately, there’s little any individual can practically do to change the course of these trends in motion.

The best you can and should do is to stay informed so that you can protect yourself in the best way possible, and even profit from the situation.

That’s precisely why bestselling author Doug Casey and his colleagues just released an urgent new PDF report that explains what could come next and what you can do about it. Click here to download it now.