{kind=link}

The Medium (of Exchange) Is the Message (on Inflation)

Does anybody keep in mind the money supply?

The idea that expansions of the cash supply fuel inflation has actually long been out of style in mainstream economics. The Federal Reserve is anchored to the notion that inflation expectations play a big function in producing actual inflation. Demand for labor is likewise extensively believed to play a leading function, possibly by providing employees with the bargaining power to require greater salaries to deal with the greater rates they anticipate. Shocks to output, of course, are believed by nearly everybody to be inflationary, a minimum of in the short-term.

Most of the argument over inflation over the previous 2 years has taken place around how much of the recent increase in rate levels was brought on by supply shocks and just how much by need shocks. Practically everybody concurs that supply restraints can cause inflation which the pandemic gave rise to diminished products of goods and services along a host of financial vectors. The plainly disputed concern was just how much of the inflation was due to output decreases and disturbances and just how much was due to stimulus-fueled excess need.

The Supply-Led Inflationist View Fell Apart

Supporters of the Biden administration and extensive financial policy have tended to argue that inflation was driven practically entirely by decreased output, supply chain interruptions, and stress caused by the sudden stops and starts to delivering around the globe. Lots of who took this position forecasted that inflation would show “transitory,” fading as output rose and supply chains cleared. The initial idea of an “immaculate disinflation” was rooted in the view that inflation would fade by itself as the supply shock fell into the rearview mirror.

(Note: we’re going to overlook of this discussion the concept that inflation was brought on by an abrupt outbreak of greed. We have it on great authority that greed is with us always. It simply feels unreasonable to pick on the greedflationists. They should have known much better, and we blame the education system and their parents for this failure.)

One of the problems with the supply-led inflationist view is that supply shocks lasted longer than many anticipated. Output from China remained much less trustworthy than people had believed due to Xi Jingping’s zero-COVID policy that locked down entire cities, including huge bases of goods manufactured for output. Russia invaded Ukraine. OPEC pressed back versus low oil prices. China’s continuous refusal to withdraw its predatory trade practices indicated Trump-era tariffs have become Biden-era policies as well. Even here in the U.S., the labor supply recuperated more gradually than anticipated, leaving lots of service sector jobs uninhabited and even manufacturing production’s recovery slow. What’s more, the Biden administration’s adherence to environment modification policymaking resulted in decreased domestic energy production.

Demand-Side Inflation More Plausible

Beyond the narrow boundaries of the Biden administration, the policy workplaces of our most left-wing senators, and exceptionally liberal corners of the ivory tower, most economists came around to the concept that excessive need was likewise playing a role. The extensive monetary policy of the Federal Reserve and the substantial fiscal deficits rung up to fight the pandemic economic crisis left Americans with excess cost savings and a bottled-up spending desires. Low levels of customer confidence were apparently overcome by the real spending by households, keeping need up.

Even among those who believed inflation was nontrivially sustained by excess need, there was a significant number who underestimated the persistence of inflation. They correctly saw that deficits had pressed demand above the economy’s capability but under-appreciated just how much of an inflationary impulse that would engender. The excess cost savings empowered strong consumer costs longer than the main stimulus programs lasted since money spent by one family ends up being another household’s income, assisting in more spending. Low levels of unemployment allowed homes to keep spending even as those cost savings decreased because there was little viewed requirement for precautionary saving.

The trustworthiness of the need story was considerably boosted by the transition of inflation from goods to services. Very little of this could be described by supply-side shocks. Instead, customer costs rotated out of products and into services, driving demand for services beyond sustainable capacity and pushing prices up. The demand-siders certainly had a more complete view of inflation than the supply-side exclusionists.

The Lonely Plowman of Quantity Theory

The most ignored perspective here was the monetarist position known as the amount theory of cash. The theory can be mentioned fairly merely: the quantity of money in blood circulation is the primary motorist of the cost level. For much of the past 2 years, the folks taking notice of the money supply– we’re thinking of John Greenwood and Steve Hanke of Johns Hopkins and Wall Street forecaster Ed Hyman of Evercore ISI– were lonely plowman in what turned out to be a forgotten and fertile field of economics.

Two years back, Greenwood and Hanke penned on op-ed for the Wall Street Journal with the prescient title “Excessive Money Hints High Inflation.” They released the quantity theory of money and M2 to forecast that the year-over-year inflation rate in the U.S. would rise to “a minimum of 6% and perhaps as high as 9%.” Which is exactly what it did over the list below year.

So, what is the quantity theory of money and M2 telling us now? For some of those who practice the dark art of counting cash, an economic downturn is long overdue. Many money supply mavens are convinced that inflation is now predestined to pull away back down to the Fed’s two percent target and possibly lower. Some say the Fed lags the curve: the real risks now are economic downturn and deflation.

We’re not persuaded. The message from the legal tender is not that economic downturn is imminent or inflation beat. It holds true that the money supply as determined by M2 is shrinking– and shrinking at a rate not seenconsidering that the 1930s. However the contraction did not begin till around last Thanksgiving. We’ve just seen below average development in the money supply given that last August. “Inflation normally lags sustained modifications in the cash supply by 12 to 24 months,” Hanke and Greenwood wrote in another Wall Street Journal op-ed. If that’s correct, we shouldn’t expect inflation to truly capitulate for at least a few more months, probably not up until next year, and maybe not up until sometime in 2025.

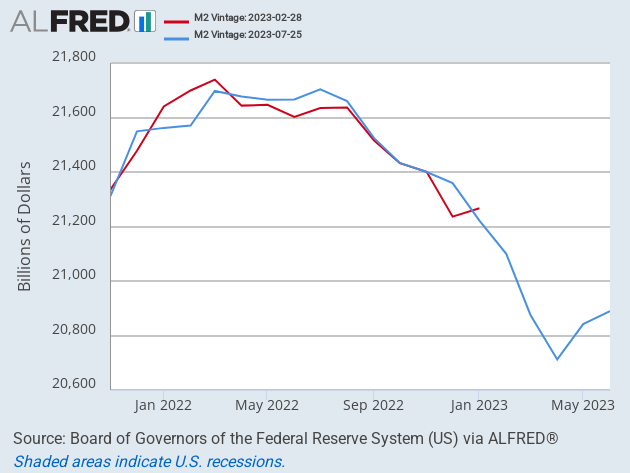

The chart above portrays the rate of change of the money supply. Our next chart shows the absolute amount of cash. Under the federal government’s initial price quotes (the red line), M2 appeared to have peaked in March of in 2015. That led lots of to believe that inflation would peak in March of this year, 12 months after peak cash supply. The blue line, however, reveals the revised quotes of M2. It explains that the cash supply peaked not in March however in July. As a result, the anticipated peak of inflation need to be numerous months later.

Notification, also, that M2 is now climbing up again. If we extend the timeline for our M2 chart, you can see that the quantity of money remains exceptionally elevated compared to the prepandemic duration. What’s more, the slump in M2 looks a lot less excellent. The cash supply is diminishing, but the majority of the motion is simply sideways. This does not look like a big disinflationary shift, much less like a trigger for deflation.

This looks to us like a story of a disinflationary impulse that might have run its course. We do not anticipate inflation to increase once again, however we would likewise not expect far more progress, based upon our reading of the amount of cash. This looks more like “peak disinflation” instead of completion of high inflation or deflation.