{kind=link}

The Fed sees itself as trapped by the incompetence and greed of the other gamers and by its own policy extremes that were little bit more than profitable “saves” of a system that is unraveling due to its fragility and brittleness.

There are two standard-issue stories about the Federal Reserve’s agenda: the Fed’s official narrative is that the Fed’s mandate is to keep inflation under control while promoting full employment. The unofficial mandate that’s obvious to all is to prop up assets, specifically the stock market, which has ended up being the Fed’s favored signifier of prosperity and the rightness/goodness of Fed policies.

The other narrative arise from “following the money”: the Fed is owned by private-sector banks, therefore behind the drape of happy-talk (complete work, blah-blah-blah), the Fed’s only real agenda is to further enrich banks and too huge to fail/jail investors– something it has managed to do with amazing success.

That the Fed inflated the 1999-2000 dot-com bubble and the 2005-2008 real estate bubble is indisputable, as is the Fed’s 2008-09 bailout of the international financial system and too big to fail/jail home loan begetters and a huge array of other profiteering, embezzler-scoundrels.

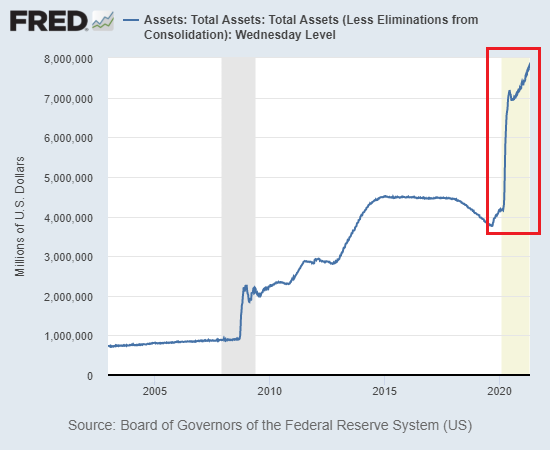

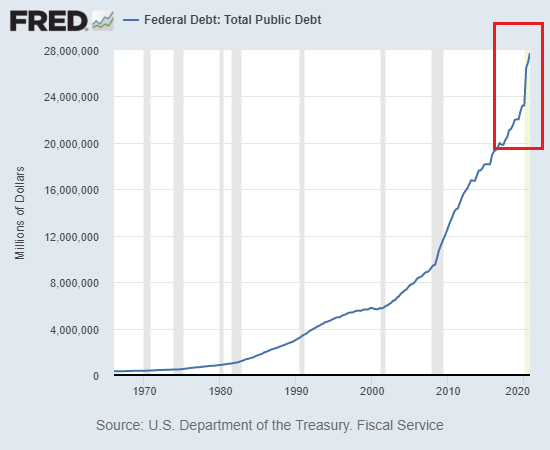

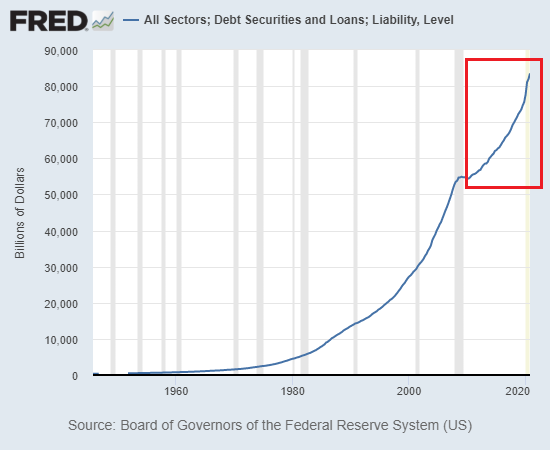

The Fed’s zero-interest rate policy (ZIRP) and extraordinary quantitative alleviating monetary stimulus have pressed the Fed balance sheet, federal financial obligation and systemic financial obligation to heights that heretofore would have been inconceivable. (Charts below)

While pursuing these non-mutually-exclusive programs–we concerned do excellent and remained to do well— the Fed has actually produced destabilizing extremes of wealth and earnings inequality, a reality that the Fed risibly rejects. (There need to be much mirth about this BS behind closed doors.)

Enable me to posit a third agenda which doesn’t negate either standard program however does explain a few of the Fed’s actions since 2008. As the system deciphers, the Fed’s main imperative is to save the financial system and economy from the greed-soaked incompetence of the other players, public and personal, by taking charge of critical swaths of the financial system and economy.

After the subprime ordeal nearly took down the entire international financial system, the Fed (with a little bit of help from Congress) basically took control of the whole $10 trillion US home loan market. Private-sector lenders had found out how to issue guaranteed-to-default home loans and pass off the deceitful mortgage-backed securities (MBS) to pension funds in Norway and an international cast of suckers who believed America’s financial system was properly controlled. (Haha, the joke’s on you.)

In reaction, the Fed generally nationalized the home loan market, buying more than $1 trillion in mortgage-backed securities and ensuring that practically all home loans in the U.S. were guaranteed or stemmed by federal companies: Fannie Mae and Freddie Mac (after their personal bankruptcy as quasi-private firms), FHA and VA.

. More recently, the Fed realized the personal broker-dealer banks that handle the all-important issuance of Treasury bonds could no longer be trusted. As this article explains, Fed Prepares To Go Direct With Liquidity, “The Fed’s main issue is not work or inflation, however rather keeping the marketplace for Treasury securities functioning.”

In response, the Fed is cutting the broker-dealers out as unreliable players. The Treasury market and the US dollar are the structures of federal spending and power, and so the Fed has actually recognized that, just as it finished with the greedy, fraudulent embezzlers of the private-sector home loan market, it needs to bypass or neuter the private-sector players as threats to stability.

Next up on the Fed’s program: organize the issuance of brand-new cash to families and cut Congress out of the loop. If you check out the Fed’s prepare for its own digital currency and the FedNow system, you’ll concern comprehend that the Fed has actually concluded that supporting usage (i.e. providing cash to homes to make it possible for more spending) is too crucial to leave in the corrupt hands of the legal bodies (Congress) or the Treasury, which need to issue financial obligation to raise money to disperse to families, financial obligation that even more strains federal profits and spending.

The Fed has actually concluded that supporting need/ intake is too essential to be left to the partisan shenanigans and pay-to-play corruption of Congress. So the Fed’s plan is to develop brand-new money out of thin air and deposit it directly in home accounts through the FedNow system.

We can’t count on you, broker-dealers or Congress, so we’re taking charge, as the system is now so over-extended that any misadventure by other players could well be catastrophic. So the only alternative from the Fed’s point of view is to take charge and cut the untrustworthy, self-serving incompetents out of the loop.

The danger of this power grab is that the Fed will misjudge the circumstance, which will prove catastrophic because the system has been stripped of strength, feedback and redundancy. I suspect the Fed sees itself as trapped by the incompetence and greed of the other gamers and by its own policy extremes that were little bit more than expedient “conserves” of a system that is unraveling due to its fragility and brittleness.

This Federal Reserve paper is common of the foundation being laid for the Fed digital currency and direct deposits to homes via FedNow accounts.

Prerequisites for a general-purpose central bank digital currency (Federal Reserve)

< img align ="center"src=" https://www.oftwominds.com/photos2021/federal-debt5-21.png "/ > If you discovered worth in this material, please join me in seeking solutions by ending up being a $1/month client of my work via patreon.com.

My brand-new book is offered! A Hacker’s Teleology: Sharing the Wealth of Our Diminishing World 20% and 15% discounts (Kindle $7, print $17, audiobook now readily available $17.46)

Read excerpts of the book totally free (PDF).

The Story Behind the Book and the Introduction.

Current Podcasts:

Beauty salon # 43: History shows again and once again how nature explains the folly of men …

Covid Has Actually Activated The Next Great Financial Crisis (34:46)

My recent books:

A Hacker’s Teleology: Sharing the Wealth of Our Shrinking World (Kindle $8.95, print $20, audiobook $17.46) Check out the first section totally free (PDF).

Will You Be Richer or Poorer?: Revenue, Power, and AI in a Shocked World

(Kindle $5, print $10, audiobook) Check out the very first area free of charge (PDF).

Pathfinding our Destiny: Avoiding the Last Fall of Our Democratic Republic ($5 (Kindle), $10 (print), ( audiobook): Read the very first area for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake $1.29 (Kindle), $8.95 (print); checked out the first chapters for free (PDF)

Cash and Work Unchained $6.95 (Kindle), $15 (print) Check out the very first area for free (PDF).

Become a $1/month client of my work through patreon.com.

KEEP IN MIND: Contributions/subscriptions are acknowledged in the order received. Your name and email remain personal and will not be provided to any other private, company or company.

|

Thank you, Roger H. ($55), for your superbly generous contribution to this website– I am significantly honored by your unfaltering assistance and readership. |

Thank you |

, Richard H. ($50), for your splendidly generous contribution to this site– I am considerably honored by your unfaltering support and readership. |