{kind=link}

All debt-fueled speculative bubbles pop, even as cheerleaders claim otherwise.

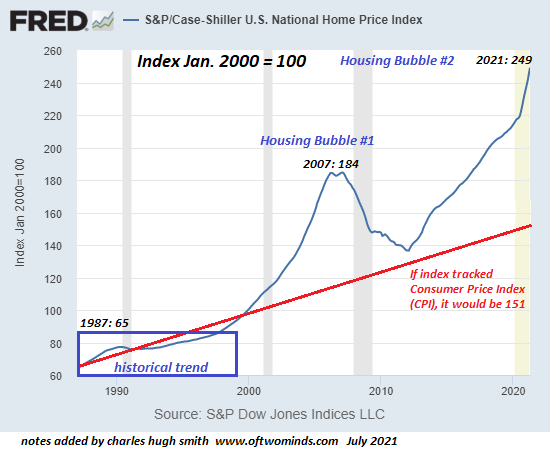

The expansion of Housing Bubble # 2 is clearly visible in these 2 charts of home valuations, courtesy of the St. Louis Federal Reserve database (FRED). The very first is the Case-Shiller Index, which as you remember tracks the rate of houses on an “apples to apples” basis, i.e. it tracks price motions for the exact same home in time.

Keep in mind that this is an index chart where the index is set at 100 as of January 2000. It is not a chart of average real estate rates.

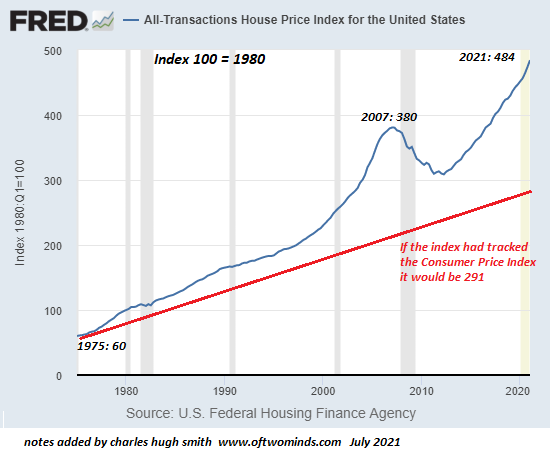

The second chart is likewise a housing rate index chart courtesy of the U.S. Federal Real Estate Finance Agency. (Shoutout to the USFHFA, never stumbled upon your work previously.)

The red line marks where home prices would be if they had actually tracked the Customer Cost Index (CPI), i.e. inflation as determined by the Bureau of Labor Data. You’ll discover that the last time the Case-Shiller Index touched this standard was 1998, nearly a quarter-century back. On the FHFA index, it hasn’t touched it since the mid-1970s, 45 years ago.

You’ll observe that real estate would need to come by 40% to touch the baseline. Yes, this is officially “difficult,” since the Fed has our back in every bubble and real estate never goes down since the need is permanently increasing.

Good, but when you turn a property class into a casino of speculators and investors having fun with Fed-spewed “free money,” you’re not dealing with shelter, you’re handling betting chips. You’ll discover that the Federal Reserve’s enormous adjustment– oops, sorry, intervention— in action to the Asian-Contagion of 1997-1998 started inflating an unmatched bubble in real estate that increased to spectacular heights on the back of Fed policies (decreasing rates of interest, and so on) and institutionalized scams on a worldwide scale in the casino’s subprime mortgage table.

You might remember that $300 billion of designed-to-default subprime mortgage pools almost took down America’s entire financial system and with that teetering, the entire worldwide monetary system ($100 trillion at the time).

I have actually frequently explained the exceptional balance of speculative bubbles popping. Housing Bubble # 1 took about four years to reach absurd evaluations and about four years to plummet towards the baseline– a decline that the Federal Reserve stopped by efficiently mingling the home mortgage market and controling home mortgage rates into a steady slide lower.

This manipulation has actually pumped up Real estate Bubble # 2 as home loan rates fell below the rate of inflation (as measured by any quasi-realistic metric). Simply put, lending institutions are losing cash on every home loan, monthly, as their yield is less than zero as soon as adjusted for inflation.

The idea that issuing mortgages that lose cash is perfectly sound and sustainable is, well, financial madness. It might be enjoyable to come from mortgages that lose money from Day One and offer them to a Norwegian pension fund or other bagholder, however with time individuals will capture on that losing cash is not a winning method in the long term.

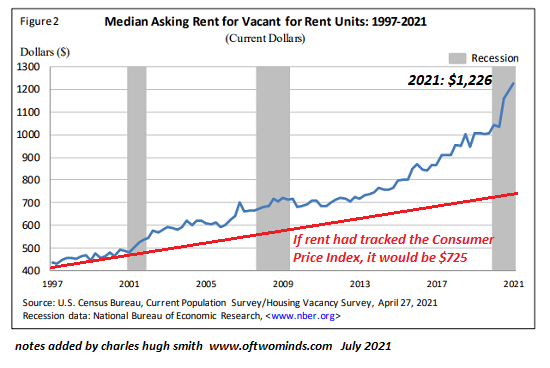

Housing Bubble # 2 has actually naturally blown a bubble in rents, as the third chart programs. If I simply paid 100% more for a rental than it deserved a couple of years back, obviously the lease should double, too, to cover my greater expenses.

To touch the baseline, rents would also need to drop 40%. yes, I know, that’s “difficult” because the Fed has our back, population is growing, and so on.

Worry of Losing Out (FOMO) is a reputable feature of every debt-funded speculative bubble and Housing Bubble # 2 has a palpable FOMO craze feel.

However housing has an intriguing function: if the variety of individuals inhabiting a dwelling increases, the population can grow by millions without requiring even one additional house. Remarkably, The variety of individuals in the average U.S. home is increasing for the first time in over 160 years (Pew Research Study).

There are 331 million U.S. residents and about 126 million occupied residences, so that has to do with 2.6 people per real estate unit.

A substantial number of the 82.5 million owner-occupied homes in America are currently occupied by one or two individuals. If the number of people residing in those houses increased, the need for extra real estate would sag significantly.

There are a consequential number of unoccupied homes in the U.S. as detailed on Page 4 of Residential Vacancies and Homeownership, Q1 2021 (Census.gov)

Many of these may be in places couple of people want to live, others might be abandoned and in need of renovation, however nevertheless it seems there are at least 5 million empty homes in the U.S. that are “held back the market” for various factors (3.8 million units) or only in “periodic use” (2 million residences that are not vacation “seasonal” homes or short-term leasings, as those are different categories).

New York City has 3.5 million real estate units and Los Angeles has 1.5 million real estate systems, so 5 million empty houses is a great deal. With more work being done from another location, and the cost of real estate at ridiculous levels in many urban areas, it’s simple to think of an increase in the number of homeowners per home and a slow migration to housing sitting empty.

I developed a micro-house back in 1978, and the pattern is accelerating. An excellent many young people can not manage a McMansion and will never be able to manage one, and lots of have no interest in debt-serfdom. Micro-houses in inexpensive backwoods are a service that adds housing units but not in the traditional high-cost manner.

All debt-fueled speculative bubbles pop, even as cheerleaders claim otherwise. There are a fantastic many people with beneficial interests in Real estate Bubble # 2 broadening forever, however history recommends a go back to the baseline is more likely than a speculative bubble broadening permanently. Need is contingent, home loan rates rest, group flows are contingent, the number of occupants per home rests, and the increase of cheap options to traditional housing is an under-appreciated pattern.

Which’s how “impossible” reverses to “inevitable.”

If you discovered value in this material, please join me in looking for services by ending up being a $1/month client of my work by means of patreon.com.

My brand-new book is available! A Hacker’s Teleology: Sharing the Wealth of Our Shrinking World 20% and 15% discounts (Kindle $7, print $17, audiobook now readily available $17.46)

Read excerpts of the book for free (PDF).

The Story Behind the Book and the Introduction.

Recent Videos/Podcasts:

It Always Ends The Same Way (34:33) (with Gordon Long)

My recent books:

A Hacker’s Teleology: Sharing the Wealth of Our Diminishing Planet (Kindle $8.95, print $20, audiobook $17.46) Check out the very first area for free (PDF).

Will You Be Richer or Poorer?: Earnings, Power, and AI in a Distressed World

(Kindle $5, print $10, audiobook) Check out the very first area free of charge (PDF).

Pathfinding our Fate: Avoiding the Final Fall of Our Democratic Republic ($5 (Kindle), $10 (print), ( audiobook): Check out the very first section free of charge (PDF).

The Adventures of the Consulting Theorist: The Disappearance of Drake $1.29 (Kindle), $8.95 (print); read the very first chapters free of charge (PDF)

Cash and Work Unchained $6.95 (Kindle), $15 (print) Read the very first section totally free (PDF).

End up being a $1/month client of my work through patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order got. Your name and email remain personal and will not be given to any other individual, business or firm.

|

Thank you, Stuart L. ($50), for your magnificently generous contribution to this website– I am greatly honored by your steadfast assistance and readership. |

Thank you |

, Hughski ($108), for your outrageously generous contribution to this website– I am considerably honored by your support and readership. |