{kind=link}

What seemed so permanent for 13 long years will be exposed as shifting sand and what appeared so real for 13 long years will be revealed as illusion. Magical thinking isn’t optimism, it is folly.

Forecasts are hard, particularly about the future, however let’s take a look at what we currently learn about 2022. Seen from Earth orbit, 2022 is Year 14 of extend and pretend and too big to stop working, too huge to jail and Year 2 of global supply chains break and energy shortages.

The essence of extend and pretend is to substitute income earned from increases in efficiency– real success– with debt– a simulation of success— that does not resolve the real problems, it simply includes a new and fatal issue: given that performance hasn’t expanded throughout the spectrum, neither has income or prosperity.

All that happened over the previous 13 years is that financial obligation– cash borrowed versus future efficiency gains and energy intake– funded illusions of success in all three sectors: households, business and government.

The explosion of debt and interest due on that financial obligation might not occur if interest rates still topped 10% as they did 40 years earlier in the early to mid-1980s. We could not add tens of trillions of dollars, yen, yuan and euros in brand-new financial obligation unless rate of interest were pushed down to near-zero (for the federal government, the wealthy and corporations only, of course– debt-serfs still pay 7%, 10%, 15%, 19%, etc)

This financial trick was achieved by making central banks the linchpin of the entire worldwide economy as reserve banks developed “money” out of thin air and utilized the currency to buy trillions in federal government and corporate bonds, synthetically developing near-infinite demand which then drove the interest rate into the ground.

Without continuous injections of more “totally free cash” and suppression of interest rates, the marketplace– oh, the scary!– would re-assert its rate discovery systems which connected interest rates to run the risk of. The expense of money is causally tied to the perceived security of the currency (i.e. danger) and the interest earned when lending it out (i.e. return or yield).

The $100 USD bill (great old Benjamin) protected from the tropic environment in a plastic bag will have more value than a 100 peso expense in any jungle on the planet because of the general perception that the Benjamin will still have considerably more value tomorrow, next month and even next year than the 100 peso note.

If danger is viewed to be higher, then rate of interest need to compensate for this risk by being much greater for risky currencies, borrowers and financial investments.

The central bank-engineered suppression of interest rates has actually damaged the market’s core system of causally linking risk and the expense of cash. Near-zero rate of interest implies near-zero danger, therefore this whole 13-year spree of suppressing the expense of money has institutionalised moral hazard, the disconnect of risk and repercussion.

The supreme artifice of extend and pretend is that threat has actually been beat: over-extended and over-leveraged debtors can constantly roll over their existing financial obligation and obtain more as ever-lower interest rates, in result paying interest with brand-new financial obligation.

Considering that danger is essentially zero, then why not make use of this chance by gaming the system? The huge gamers who broke the laws against expert trading, selling securities developed to stop working, etc, discovered that the global Empire of Debt viewed prosecuting monetary criminal activities as potentially upsetting, so not just did risk fall to zero, so did the consequences of scams, collusion and impropriety.

And because the bigger players had endless access to reserve bank credit, their bets quickly ended up being so risky and so large that the entire monetary system became fragile and susceptible to cascading collapse. Central banks and state treasuries were required to bail out the most outright criminal firms and neglect the criminality of people in those firms, institutionalising too big to fail, too big to prison.

The really interesting thing here is that the stability of any system depends upon precisely what reserve banks have snuffed out: a transparent market that rates risk within the restraints of effects. Over the previous 13 years, the invulnerability and rewards bestowed on those who borrowed to the hilt and after that borrowed much more and put all the main bank-issued “money” on leveraged bets has dripped into the awareness of retail punters, people, households and small bettors, oops, I mean investors.

With genuine efficiency and profits stagnant and all the gains of video gaming the central bank’s suppression of danger flowing to the leading 0.1%, the commoners have actually now followed the Nobility into the gambling establishment. Wealth is no longer perceived as flowing from efficiency but from speculation and the jumping from one property bubble to the next.

Considering that increasing efficiency can not be made risk-free while speculation can be made to appear risk-free for a time, all the money and talent has actually streamed into speculation. The real life decomposes away as everyone pursues the incentives that the reserve bank routine have developed to game the monetary system and hypothesize as hugely as you can because there’s no longer any risk of any possession ever declining ever again.

The reserve bank program incentivized speculation by rewarding those who borrowed and leveraged the greatest bets. In the central bank gambling establishment, everyone who bets on possession bubbles broadening to the sky is a winner. Anyone who took real-world risks by investing in the production of goods and services was a loser.

I frequently describe first-order and second-order impacts, and that’s the story that will be told in 2022 with explosive results. First-order effects: actions have repercussions. Second-order results: those consequences have repercussions.

The first-order effects of reserve banks’ suppression of rates and danger were amazingly satisfying: assets soared to ever greater highs and enough of the flood of new credit reached the masses to stimulate an orgy of consumption paid not by profits and performance however by financial obligation. Corporations didn’t improve performance, they borrowed billions and redeemed their own shares, reducing the float and therefore generating higher profits per share.

But the new incentive structure generated by this damage of market characteristics ruined not simply rate discovery of threat, it likewise destroyed the structure of real prosperity: investing in increasing efficiency rather than in speculative gains.

The Federal Reserve managed to suppress interest rates but it doesn’t control danger or effect. On the systems level, all that reserve banks accomplished was to move all the risk accumulating as an effect of their incentivizing of speculation to the entire monetary system itself.

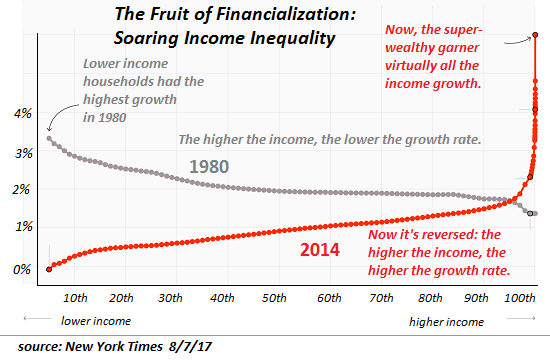

By incentivizing speculation and feeding the belief that possessions can never decrease, the central banks have implicitly made a pledge they can not keep: consequences have actually been snuffed out together with threat. One repercussion of incentivizing speculation and backstopping the biggest gamers’ bets is that the biggest players have actually garnered the large majority of the gains (see chart below). This vast differential has generated extraordinary wealth inequality, a concentration of wealth in the hands of the couple of at the cost of the lots of that has actually completely corrupted the nation’s political and social orders.

2022 is the year that the second-order results come home to roost: all the risk that has been transferred to the financial system as a whole will produce repercussions the Fed and other central banks are unable to control. The stupendously toxic incentives to hypothesize will produce consequences the Fed and other reserve banks are not able to control. The stupendously hazardous wealth inequality will create consequences the Fed and other reserve banks are not able to manage.

The hubris and magical thinking of the main lenders has actually infected the whole population, most of whom now confuse wonderful thinking with optimism. The belief that central banks can snuff out danger and consequence and the second-order results of those consequences is wonderful thinking. The belief that possession bubbles will keep expanding due to the fact that of the omnipotence of central banks is wonderful thinking. The belief that success is the outcome of shifting bets from one video gaming table to the next is wonderful thinking. The belief that central banks have god-like powers and nothing can restrict their power is wonderful thinking.

The funny feature of system dynamics is they do not react to what we like, want or think. Thinking that reserve banks can make the monetary system and economy do whatever they want does not imply they really have that power. Thinking that second-order impacts have been snuffed out doesn’t indicate they’ve in fact been extinguished.

What will amaze us in 2022 is the exposure of reserve banks’ limitations of power and the explosive effects of second-order impacts. What seemed so permanent for 13 long years will be exposed as shifting sand and what seemed so real for 13 long years will be exposed as illusion. Magical thinking isn’t optimism, it is recklessness.

My brand-new book is now readily available at a 20 % discount rate this month: Global Crisis, National Renewal: A(Revolutionary)Grand Method for the United States(Kindle$8.95, print$20)If you discovered worth in this material, please join me in looking for options by ending up being a$1/month customer of my work via patreon.com. Recent Videos/Podcasts: The Central Bank System Has Failed, It’s Time To Redraw America’s Grand Technique (39 min) Jay Taylor and I talk about why Inflation is a Runaway Freight Train( 21 minutes)A Grand Method to Deal With the Global Crisis(54 min., with Richard Bonugli) XI’s GAMBIT:A

Bridge Too Far?(41 min, with Gordon Long)

States(Kindle$ 9.95, print $25 )Read Chapter One totally free (PDF). A Hacker’s Teleology: Sharing the Wealth of Our Shrinking World(Kindle$8.95, print$20, audiobook$17.46)Check out the first section free of charge (PDF). Will You Be Richer or Poorer?: Earnings, Power, and AI in a Distressed World( Kindle$5, print$10, audiobook)Check out the very first area free of charge (PDF ). Pathfinding our Destiny: Avoiding the Last Fall of Our Democratic Republic($5 Kindle

, $10 print, (audiobook): Check out the very first section totally free(PDF). The Adventures of the Consulting Theorist: The Disappearance of

Drake$1.29 Kindle,$8.95 print); read the first chapters totally free (PDF)Money and Work Unchained $6.95 Kindle,$15 print)Read the first area totally free Become a$1/month patron of my work via patreon.com. KEEP IN MIND: Contributions/subscriptions are acknowledged in the order received. Your name and email stay private and will not be offered to any other private, business or firm. Thank you, Mark H.($50), for your superbly generous contribution to this website– I am greatly honored by your unfaltering assistance and readership. Thank you, Kevin S. ($50), for your splendidly generous contribution to this site– I am significantly honored by your support and readership. Thank you, Samuel T.($20), for your most-excellently generous contribution to this site– I am significantly honored by your steadfast support and readership. Thank you, Stephen P.($54), for your awesomely generous contribution to this site– I am significantly honored by your support and readership.